پرونده:Subprime crisis - Foreclosures & Bank Instability.png

{kind=link}

{kind=link}

{kind=link}

پروندهٔ اصلی (۹۶۰ × ۷۲۰ پیکسل، اندازهٔ پرونده: ۱۶ کیلوبایت، نوع MIME پرونده: image/png)

این پرونده در ویکیانبار موجود است. محتویات صفحهٔ توصیف آن در زیر نمایش داده میشود. |

{kind=link}

|

این diagram نگاره میبایست با استفاده از گرافیک برداری اسویجی فایل بازسازی شوند. این چند مزیت دارد؛ Commons:Media for cleanup را برای اطلاعات بیشتر ببینید. اگر حالت برداری آن در حال حاضر موجود است، لطفاً آن را بار کنید. پس از بارکردن یک اسویجی، این الگو را با {{vector version available|new image name.svg}} جایگزین کنید.

|

| توضیح |

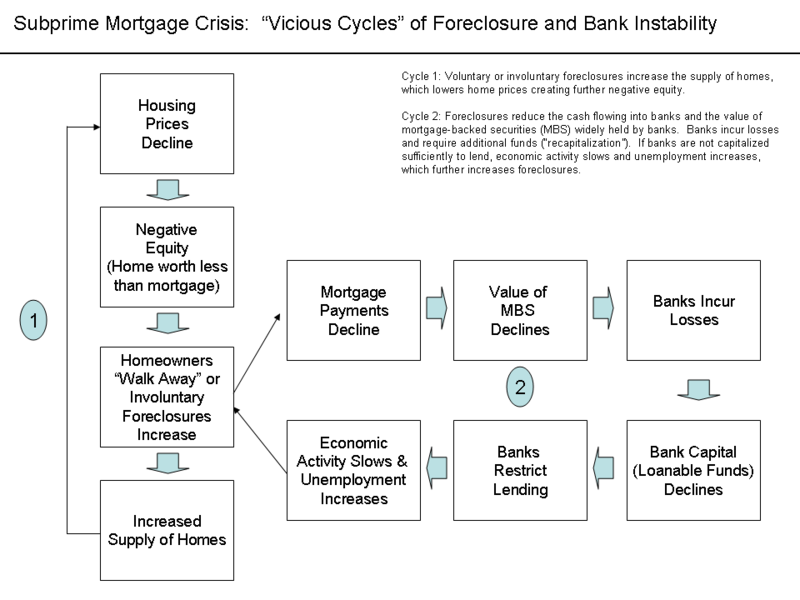

English: Chart showing feedback loops within housing market and with financial market and economy خلاصهThis diagram explains two vicious cycles at the heart of the subprime mortgage crisis. Cycle One: Housing MarketThe first cycle is within the housing market. Voluntary or involuntary foreclosures increase the supply of homes, which lowers home prices creating further negative equity. By September 2008, average U.S. housing prices had declined by over 20% from their mid-2006 peak.[1][2] This major and unexpected decline in house prices means that many borrowers have zero or negative equity in their homes, meaning their homes were worth less than their mortgages. As of March 2008, an estimated 8.8 million borrowers — 10.8% of all homeowners — had negative equity in their homes, a number that is believed to have risen to 12 million by November 2008. Borrowers in this situation have an incentive to "walk away" from their mortgages and abandon their homes, even though doing so will damage their credit rating for a number of years. The reason is that unlike what is the case in most other countries, American residential mortgages are non-recourse loans; once the creditor has regained the property purchased with a mortgage in default, he has no further claim against the defaulting borrower's income or assets. As more borrowers stop paying their mortgage payments, foreclosures and the supply of homes for sale increase. This places downward pressure on housing prices, which further lowers homeowners' equity. The decline in mortgage payments also reduces the value of mortgage-backed securities, which erodes the net worth and financial health of banks. This vicious cycle is at the heart of the crisis.[3] Cycle Two: Financial Market and Feedback into Housing MarketForeclosures reduce the cash flowing into banks and the value of mortgage-backed securities (MBS) widely held by banks. Banks incur losses and require additional funds (“recapitalization”). If banks are not capitalized sufficiently to lend, economic activity slows and unemployment increases, which further increases foreclosures. As of August 2008, financial firms around the globe have written down their holdings of subprime related securities by US$501 billion. Mortgage defaults and provisions for future defaults caused profits at the 8533 USA depository institutions insured by the FDIC to decline from $35.2 billion in 2006 Q4 billion to $646 million in the same quarter a year later, a decline of 98%. 2007 Q4 saw the worst bank and thrift quarterly performance since 1990. In all of 2007, insured depository institutions earned approximately $100 billion, down 31% from a record profit of $145 billion in 2006. Profits declined from $35.6 billion in 2007 Q1 to $19.3 billion in 2008 Q1, a decline of 46%. Federal Reserve data indicates banks have significantly tightened lending standards throughout the crisis.[4] Unemployment in the U.S. has increased to a 14-year high as of November 2008.[5] Further Sources and SolutionsEconomist Nouriel Roubini described the vicious cycles within and across the housing market and financial markets during interviews with Charlie Rose in September and October 2008.[6] He further describes the crisis in these other video segments.[7][8] He called for an additional $250 billion to help recapitalize the banks, closure of insolvent "zombie" banks, regulatory overhaul, and $300 billion in infrastructure spending during these interviews. ReferencesSee alsoThe images below contain additional high-level explanation of the crisis further citations. thumb|Factors Contributing to Housing Bubble – Diagram 1 of 2 thumb|Domino Effect As Housing Prices Declined – Diagram 2 of 2 |

| تاریخ | |

| منبع | اثر شخصی (متن اصلی: «I created this work entirely by myself.») |

| پدیدآور | Farcaster (talk) 17:06, 26 December 2008 (UTC) |

{kind=link}

{kind=link}

- ↑ Case Shiller Index

- ↑ Economist-A Helping Hand to Homeowners

- ↑ NYT - How to Help People Who's Homes are Underwater

- ↑ Banks Tighten Lending Standards

- ↑ https://www.nytimes.com/2008/11/08/business/economy/08econ.html?pagewanted=print NY Times - Unemployment]

- ↑ Charlie Rose - Roubini & Panel

- ↑ Rose & Roubini Discussion

- ↑ Rose & Roubini

اجازهنامه

- شما اجازه دارید:

- برای به اشتراک گذاشتن – برای کپی، توزیع و انتقال اثر

- تلفیق کردن – برای انطباق اثر

- تحت شرایط زیر:

- انتساب – شما باید اعتبار مربوطه را به دست آورید، پیوندی به مجوز ارائه دهید و نشان دهید که آیا تغییرات ایجاد شدهاند یا خیر. شما ممکن است این کار را به هر روش منطقی انجام دهید، اما نه به هر شیوهای که پیشنهاد میکند که مجوزدهنده از شما یا استفادهتان حمایت کند.

- انتشار مشابه – اگر این اثر را تلفیق یا تبدیل میکنید، یا بر پایه آن اثری دیگر خلق میکنید، میبایست مشارکتهای خود را تحت مجوز یکسان یا مشابه با ا اصل آن توزیع کنید.

|

اجازهٔ کپی، پخش و/یا تغییر این سند تحت شرایط مجوز مستندات آزاد گنو، نسخهٔ ۱٫۲ یا هر نسخهٔ بعدتری که توسط بنیاد نرمافزار آزاد منتشر شده؛ بدون بخشهای ناوردا (نامتغیر)، متون روی جلد، و متون پشت جلد، اعطا میشود. یک کپی از مجوز در بخشی تحت عنوان مجوز مستندات آزاد گنو ضمیمه شده است. |

سیاهه بارگذاری اصلی

{kind=link}

- 2008-12-26 17:34 Farcaster 960×720× (16380 bytes)

- 2008-12-26 17:29 Farcaster 960×720× (16314 bytes)

- 2008-12-26 17:06 Farcaster 960×720× (16314 bytes) {{Information |Description=Chart showing feedback loops within housing market and with financial market and economy |Source=I created this work entirely by myself. |Date= |Author=~~~~ |other_versions= }}

تاریخچهٔ پرونده

روی تاریخ/زمانها کلیک کنید تا نسخهٔ مربوط به آن هنگام را ببینید.

| تاریخ/زمان | بندانگشتی | ابعاد | کاربر | توضیح | |

|---|---|---|---|---|---|

| کنونی | ۱۴ اکتبر ۲۰۱۰، ساعت ۰۰:۵۱ | | ۹۶۰ در ۷۲۰ (۱۶ کیلوبایت) | Hideokun | {{Information |Description={{en|Chart showing feedback loops within housing market and with financial market and economy<br/> ==Description== This diagram explains two vicious cycles at the heart of the [[:en:subprime mortgage crisis |

کاربرد پرونده

صفحهٔ زیر از این تصویر استفاده میکند:

کاربرد سراسری پرونده

ویکیهای دیگر زیر از این پرونده استفاده میکنند:

- کاربرد در en.wikipedia.org

- کاربرد در hi.wikipedia.org

- کاربرد در ja.wikipedia.org

- کاربرد در pt.wikipedia.org

- کاربرد در ta.wikipedia.org

{kind=link}